Photo Credit: OpenIDEO

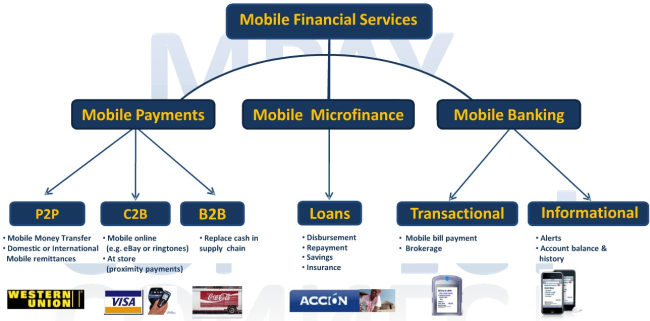

According to article released this week by Uganda Online, hospitals in Uganda are now accepting mobile money to pay for health expenses. While there are eight mobile providers in Uganda, four are providing mobile money services to their customers – MTN’s MobileMoney, Airtel’s ZAP, UTL’s M-Sente and Warid Pesa – with Orange Uganda planning on releasing their version of the service soon. In the article, a picture clearly shows that the hospital (Case Clinic) allows for mobile payments from MTN and Airtel. Other companies in Uganda are allowing for mobile payments – DStv (satellite TV provider), NWSC (water and sewerage) and Umeme (energy provider).

Utilizing mobile money in the health sector is nothing new. M-PESA in Tanzania has been used by the CCBRT Hospital to pay for patients’ bus ticket from rural areas to the hospital’s location in Dar es Salaam (the capital city). In Kenya, Changamka allows individuals to save and pay for health services by combining a medial smart card with M-PESA. In the Philippines, Smart Communications has partner with PhilHealth, a national insurance provider, to allow customers to pay their premiums via mobile money. This list continues as money mobile is being further employed in the health sector which includes insurance, vouchers program, and conditional cash transfers. The ability to save and pay via mobile money for health issues creates insurance for individuals and families that do not have access to typical insurance products. Mobile money has also been leveraged to pay nurses and community health workers serving in rural areas which helps with worker retention and decreases tardiness.

In the mHealth sector, this is a clear sign that innovative solutions can be shaped around current mobile products and services. Once mobile money has been established in countries, this opens doors for new businesses to be developed around the mobile money platform. The examples above show the need and desire for products that create the ability to both save and pay for health service. While the Ugandan example is not a revolutionary app (or killer app), it provides a necessary product so individuals and families can receive curial medical services. In this case, the ‘killerness’ of the service to using mobile money in the health care system is that it fits both the needs and infrastructure of Uganda, include accepting payments from multiple mobile providers.

A recent study reveals how Information and Communication Technology (ICT) can viably provide access to education, healthcare, agro-services and financial services to the Base of the Pyramid (BoP). The study reviewed more than 280 initiatives set up by various types of actors (corporations, Citizen Sector Organizations, social entrepreneurs…) in Asia, Latin America and Africa which are using ICTs to provide services to the BoP.

A recent study reveals how Information and Communication Technology (ICT) can viably provide access to education, healthcare, agro-services and financial services to the Base of the Pyramid (BoP). The study reviewed more than 280 initiatives set up by various types of actors (corporations, Citizen Sector Organizations, social entrepreneurs…) in Asia, Latin America and Africa which are using ICTs to provide services to the BoP.

As the global population continues to grow – it is expected to reach more than 9 billion by 2050. It will require a 70% increase in food production above current levels. Most of this increased yield will have to be achieved in less developed countries (LDCs), many of whose farmers operate on a small scale and are highly exposed to crop failure and adverse commodity price movements. This month, Vodafone, Accenture and Oxfam released a report on mAgriculture. The report titled “

As the global population continues to grow – it is expected to reach more than 9 billion by 2050. It will require a 70% increase in food production above current levels. Most of this increased yield will have to be achieved in less developed countries (LDCs), many of whose farmers operate on a small scale and are highly exposed to crop failure and adverse commodity price movements. This month, Vodafone, Accenture and Oxfam released a report on mAgriculture. The report titled “

")

")

")

")

")

")

")

")

")

")

")